The World Economic Forum Global Risks Report 2026 outlined a clear shift: the global system is moving away from cooperation and efficiency toward fragmentation, competition, and resilience. At the time, this was presented as a forward-looking risk framework. Two months into 2026, it is already visible in real-world developments.

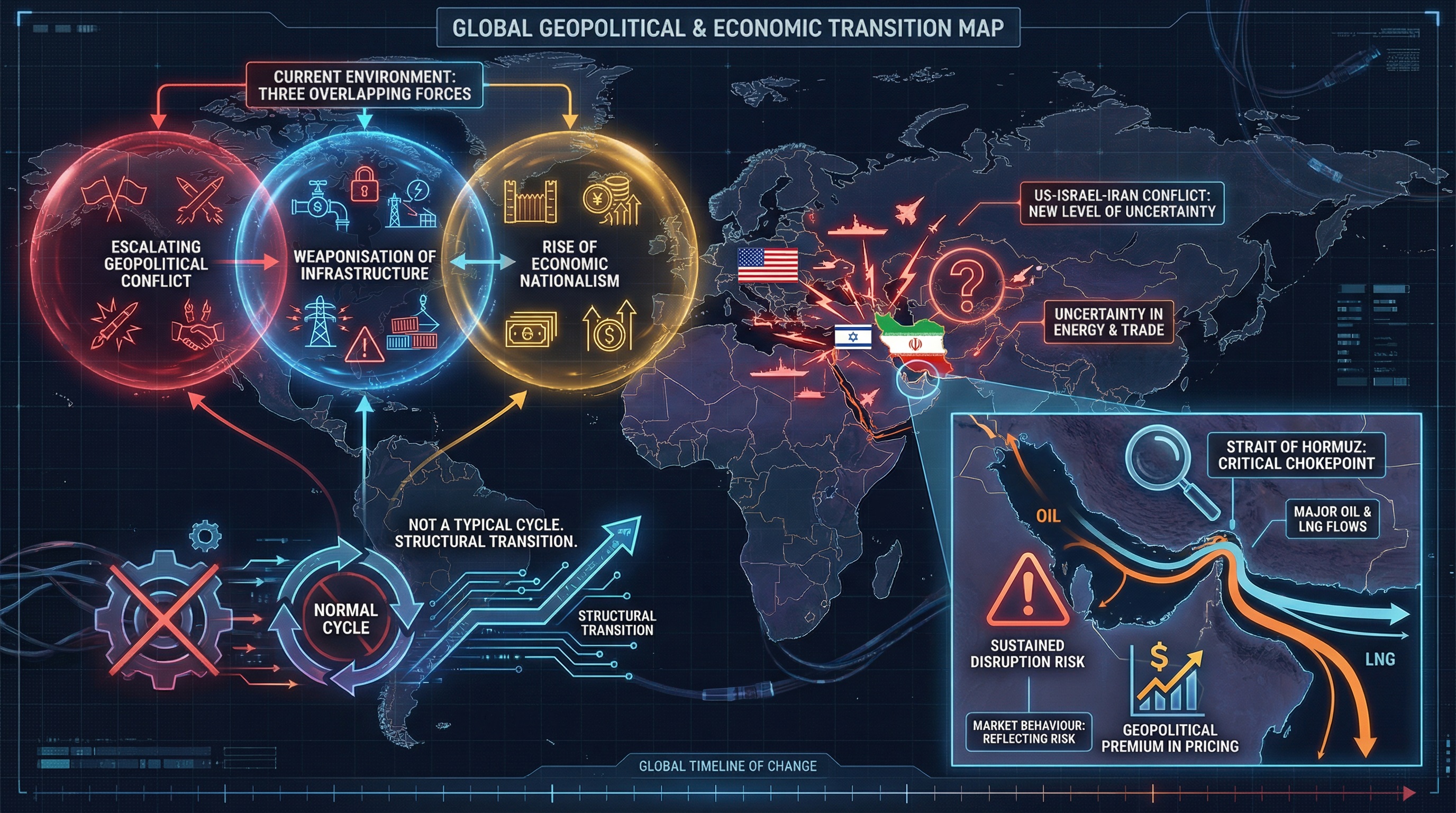

The current environment is defined by three overlapping forces: escalating geopolitical conflict, the weaponisation of infrastructure, and the steady rise of economic nationalism.

These are no longer isolated risks. They are interacting in ways that directly influence capital markets, asset pricing, and investor behaviour.

For investors, the key takeaway is simple. This is not a typical cycle that will revert back to normal.** It is a structural transition**, and it requires a different way of thinking about capital allocation.

Connect with our experts** to position your portfolio for resilience and opportunity in the current environment.**

From Globalisation to Strategic Fragmentation

For decades, global markets operated on a relatively stable model. Supply chains were optimised for cost, capital moved freely across borders, and geopolitical tensions were largely contained within regional boundaries. That model is now breaking down.

Governments are increasingly prioritising national security and economic resilience over efficiency. This is visible in the reshoring of manufacturing, the introduction of tariffs and export controls, and the growing alignment between economic policy and geopolitical strategy.

The World Economic Forum defines this as geoeconomic confrontation, and it is now one of the most significant risks facing the global economy.

This shift is changing how the real economy functions:

- Supply chains are being** redesigned for reliability rather than cost**

- Inventory levels are increasing to protect against disruption

- Trade flows are becoming more regionalised

The result is a system that is inherently less efficient but more resilient. However, that resilience comes at a cost.

Inflation becomes more persistent, margins become tighter, and volatility becomes a permanent feature of markets rather than a temporary disruption.

Strategic implication:** **Markets are no longer driven purely by growth. They are increasingly driven by risk management at a national level.

The Middle East: Where Geopolitics Meets Markets

The current escalation in the Middle East is one of the clearest examples of how geopolitical risk is now feeding directly into financial markets. The conflict involving the United States, Israel, and Iran has introduced a new level of uncertainty, particularly across energy markets and trade routes.

The most immediate transmission mechanism is energy. The Strait of Hormuz remains one of the most critical chokepoints globally, with a significant portion of oil and LNG flows passing through it. Any** sustained disruption introduces a geopolitical premium into pricing, which is already being reflected in market behaviour**.

This is visible in several ways:

- Oil prices** are being supported by risk**, not just supply-demand fundamentals

- Shipping and insurance costs are rising due to perceived threat levels

- Energy-importing economies are facing renewed inflation pressure

This reinforces a structural shift: energy is no longer behaving as a purely cyclical commodity. It is increasingly priced as a strategic asset influenced by geopolitical risk.

A parallel development is emerging in the digital layer of the economy. Recent strikes on cloud data centres in the UAE highlight a shift in how modern economies can be disrupted.

Digital infrastructure is no longer treated as commercially neutral. It is increasingly viewed as part of a country’s critical infrastructure. Because it underpins banking systems, payment networks, and corporate operations, any disruption can have immediate and system-wide economic effects,** extending well beyond the initial target**.

Strategic implication: Geopolitical risk now transmits through both energy systems and digitally integrated infrastructure, affecting markets more quickly and more broadly than in previous cycles.

To reassess your portfolio in light of rising geopolitical risk across energy and infrastructure, connect with our experts. We can help position your capital for the current environment.

Digital Infrastructure and the Shift Toward Sovereign Systems

While the events in the Middle East illustrate how digital infrastructure can be disrupted, the more important development is structural rather than event-driven.

Rather than being treated as globally neutral platforms, digital infrastructure is increasingly being brought under national control. Governments are recognising that systems underpinning finance, data, and communications cannot remain fully exposed to external dependencies.

This is changing how digital infrastructure is deployed and managed:

- Data centres are being aligned with national or regional jurisdictions

- Cloud infrastructure is increasingly localised or duplicated across regions

- **Regulatory oversight is expanding **over data, storage, and access

Financial systems are also evolving in parallel. There is a growing effort to reduce reliance on external payment networks and financial rails, particularly those exposed to geopolitical influence.

This is leading to a more regionalised structure:

- Payment systems are becoming more** locally controlled**

- Data governance tied to jurisdictional boundaries

- Capital flows are becoming more selective and regulated

Strategic implication: What began as a vulnerability is now accelerating a shift toward sovereign control of digital and financial systems, reinforcing the broader move toward a fragmented global framework.

US–China Relations: Stability Without Resolution

Despite broader global volatility, the relationship between the United States and China remains relatively stable at a surface level. Diplomatic engagement continues, and both sides recognise the importance of maintaining economic ties.

However, the underlying structural tensions remain unresolved. Key areas of friction include:

- Technology restrictions and export controls

- Industrial overcapacity in sectors like EVs and solar

- Competition over supply chain dominance

The result is not full decoupling, but a more selective form of integration. Countries are cooperating where necessary, but competing where it matters strategically.

Strategic implication:** **The base case is not conflict or cooperation—it is managed competition with persistent friction.

Russia–Ukraine: Conflict as a Structural Baseline

The war in Ukraine has now moved beyond being a defining shock event. It has become part of the structural backdrop of the global economy. The conflict continues to influence energy markets, agricultural supply chains, and defence spending.

One of the most important aspects of this conflict is the continued targeting of infrastructure. Energy grids, logistics networks, and industrial facilities continue to be primary targets.

This reinforces a broader theme seen across multiple regions: infrastructure is both a vulnerability and a strategic asset.

Strategic implication:*** ***This is not a temporary disruption. It is a persistent condition that must be priced into markets.

The Economic Layer: Debt, Inflation, and Asset Stability

The World Economic Forum highlights the risk of an economic reckoning driven by three interconnected factors: debt, inflation, and asset valuations. These pressures are now beginning to surface.

Global debt levels remain high, while interest rates are no longer anchored at historic lows. This creates refinancing risk and limits the ability of governments to respond to future shocks.

At the same time, inflation has become more complex. It is now driven by supply constraints, energy volatility, and policy intervention, rather than purely by demand.

This has direct implications for asset markets:

- Valuations supported by low interest rates are under pressure

- Liquidity is less predictable

- Returns are becoming more dependent on underlying cash flow

Strategic implication:** **The market environment is shifting from liquidity-driven returns to fundamentals-driven returns.

*Source: *World Economic Forum

Investor Strategy: Protecting and Growing Capital in an Era of Geopolitical Risk

In this environment, investors need to move away from traditional models built on stability and efficiency. The focus should shift toward resilience, cash flow, and strategic positioning.

The first priority is to anchor portfolios in assets that are tied to essential economic activity. These assets are less sensitive to external shocks and more likely to maintain demand.

Core areas to prioritise:

- Infrastructure (energy, transport, utilities)

- Logistics and industrial real estate

- Income-producing real estate with strong tenant demand

Energy exposure is also critical. In the short term, oil and gas markets will continue to reflect geopolitical risk. Over the longer term, investment in energy infrastructure—particularly grid systems and nuclear—will become increasingly important.

At the same time, risk needs to be managed more carefully. Highly leveraged strategies and speculative assets are more vulnerable in a volatile environment. Reducing exposure to these areas and focusing on strong balance sheets is essential.

Key risk management principles:

- Prioritise cash-flow-generating assets

- Limit reliance on leverage

- Maintain liquidity for flexibility

Inflation must also be addressed directly. Assets with pricing power—such as real estate with shorter lease cycles or infrastructure with indexed contracts—provide a degree of protection.

Geography plays an increasingly important role in the current environment. Capital should be allocated to regions that offer stability, strong regulatory frameworks, and strategic relevance within global trade and supply chains. In a fragmented system,** priority should shift toward jurisdictional resilience rather than simply targeting growth**.

Finally,** volatility itself creates opportunity**. Periods of market stress often lead to mispricing and forced selling. Investors with available capital are in a position to take advantage of these situations.

Where opportunities are emerging:

- Distressed or secondary real estate markets

- Developer inventory under liquidity pressure

- Private transactions with motivated sellers

A Practical Portfolio Structure

To translate this into action, portfolios should be structured across three clear layers:

1. Protection

- Cash and liquidity

- Precious metals

- Low-risk income assets

2. Stability

- Infrastructure

- Prime real estate

- Logistics and industrial assets

3. Upside

- Select growth sectors such as AI

- Opportunistic investments during dislocation

This structure allows investors to balance downside protection with the ability to capture opportunities.

Conclusion: What the WEF Global Risks Report 2026 Confirms

The events of early 2026 confirm the core message of the Global Risks Report.** The global system is transitioning toward fragmentation, competition, and increased volatility. Trade is becoming more regional, infrastructure is being securitised, and technology is increasingly tied to national interests**.

For investors, this is not a period to wait for stability to return. It is a period to adapt. Those who focus on resilience, cash flow, and strategic positioning will be better placed to navigate the uncertainty ahead. Those who continue to rely on the assumptions of the past are likely to face increasing challenges.

The environment is shifting, and your strategy should adapt with it. Book a consultation with our specialists to strengthen resilience and position your portfolio for the current cycle.

This article is for general information only and does not constitute financial, legal or tax advice. Rules, prices and regulations change; verify current requirements with a qualified adviser before acting.