*Photo: Gage Skidmore via *Wikimedia Commons

{kind=link}

When U.S. President Donald Trump announced plans late last week to impose 100 percent tariffs on Chinese imports, global markets moved as if an entirely new trade war had begun overnight. The statement, delivered after China expanded its own export controls on rare-earth minerals, set off a swift chain reaction across equity markets.

Immediate Market Impact After Trump's Tariff Threat

By Friday’s close, the S&P 500 had dropped 2.7 percent and the Nasdaq Composite fell 3.6 percent — their sharpest single-day losses since April. The Dow Jones Industrial Average shed nearly 900 points, or 1.9 percent.

When Asian markets opened Monday, the selling extended:

- Hong Kong’s Hang Seng Index fell 1.7 percent, led by Chinese financial and technology shares.

- South Korea’s KOSPI declined 0.7 percent.

- Australia’s ASX 200 lost 0.8 percent.

- Mainland China’s Shanghai Composite slipped 0.2 percent.

Meanwhile, European equities showed smaller declines before stabilizing. Germany’s DAX traded 0.5 percent higher by midday Monday and France’s CAC 40 gained 0.7 percent, indicating that investors there saw limited spill-over risk.

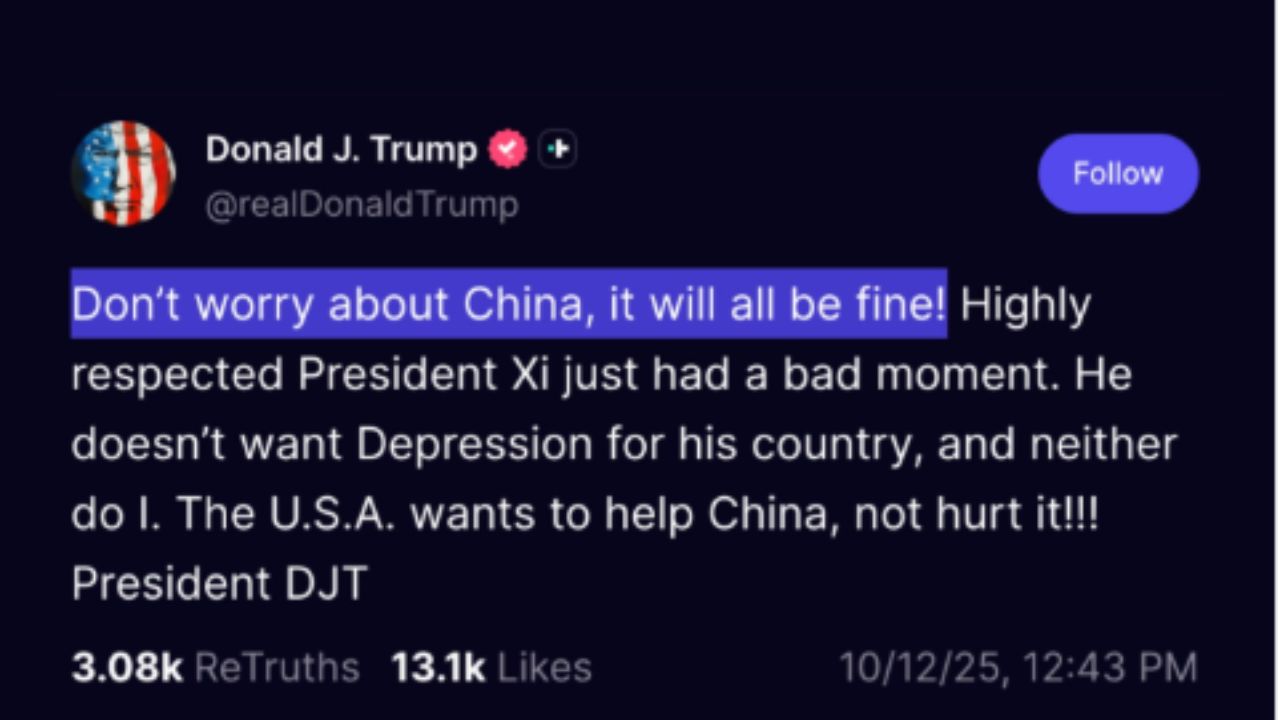

The U.S. futures market rebounded Sunday night after Trump wrote on Truth Social that America “wants to help China, not hurt it,” suggesting flexibility on the timing or scope of the tariffs.

By early Monday morning Eastern Time, Dow futures were up 1.1 percent, the S&P 500 1.5 percent, and the Nasdaq 2 percent.

In other words, within less than three days, sentiment swung from sharp risk-off to partial recovery — with no substantive change in trade policy or economic data between the two points.

What Triggered the Announcement

Trump’s statement followed Beijing’s decision to tighten control over rare-earth exports, a move Chinese officials described as a “legitimate national-security measure.” Rare earths are used in everything from smartphones and electric motors to missile guidance systems.

China processes roughly 90 percent of the world’s rare-earth materials and produces over 80 percent of global permanent magnets. The new rules, which include additional export-license scrutiny, are scheduled to take effect in November.

Washington viewed the step as potentially coercive, given that the U.S. had introduced its own restrictions on chipmaking and AI-related exports to China only weeks earlier. Trump’s tariff threat was presented as a countermeasure, intended to “defend American industry” if Beijing’s controls disrupted supply chains.

However, no formal tariff schedule has been filed with the Office of the U.S. Trade Representative, and officials have indicated that negotiations remain ongoing.

Assessing the Magnitude

If enacted as described, a 100 percent surcharge on Chinese imports would raise average U.S. tariff levels on Chinese goods to about 130 percent, close to the 145 percent peak reached during the height of the spring 2025 tariff confrontation.

According to U.S. Census Bureau data, imports from China totaled $427 billion in 2024, meaning a full tariff implementation could theoretically affect more than $400 billion of trade.

But that figure assumes all products are subject to the new rate, which rarely occurs in practice. During the previous trade-war phase, actual effective tariffs covered about 60 percent of Chinese imports, and many were later suspended.

The Pattern of Headline-Driven Volatility

Episodes like this have become frequent in the last decade. Studies by the Federal Reserve Bank of San Francisco and others have shown that algorithmic trading and headline-based models amplify intraday reactions to political or policy statements.

When language in official remarks contains high-volatility keywords — such as “tariffs,” “sanctions,” or “retaliation” — automated systems can drive outsized price swings before human analysis rebalances sentiment.

The result is visible here: a reflexive correction detached from measured changes in trade probability.

Investor Positioning

Options data from the Chicago Board Options Exchange on Friday showed a spike in put-call ratios, indicating short-term hedging rather than long-term repositioning. ETF flow data, meanwhile, showed minimal outflows from major equity funds, reinforcing the interpretation that institutions viewed the drop as tactical, not structural.

Similarly, U.S. Treasury yields declined modestly, and gold rose 1.4 percent — classic “risk-off” signals, but on a moderate scale compared with true crisis episodes.

Comparing Past Precedents

In 2018–2019, during the original U.S.–China tariff cycle, the S&P 500 experienced four separate declines of more than 2 percent following tariff tweets or press briefings. Each time, losses were recouped within roughly two weeks after clarifying statements or partial rollbacks. Economic growth slowed temporarily but did not enter recession.

Those precedents suggest that headline-driven sell-offs tend to correct once policy clarity returns.

Short-Term Implications

For now, the risk to corporate earnings and supply chains remains theoretical. The probability of full implementation will depend on upcoming bilateral discussions and whether Beijing enforces its rare-earth restrictions strictly or administratively delays licenses without an outright ban.

Until those details emerge, markets are operating on speculation rather than quantifiable policy.

Political Calculus Behind the Tariff Threat

While market participants focused on the headline number — “100 percent tariffs” — the context points to a negotiation strategy rather than an imminent policy. U.S. officials familiar with the matter, speaking to several media outlets, indicated the announcement was designed to signal leverage ahead of another round of trade discussions rather than to introduce immediate measures.

Historically, Trump has used tariff declarations as bargaining tools. During the 2018-2019 trade war, multiple proposed duties were delayed, modified, or canceled once talks advanced. Out of the 25 separate tariff notices issued in that period, fewer than half took full effect.

Domestic politics also play a role. The administration faces a tightening budget cycle and an election year approaching. Reasserting pressure on China resonates with part of Trump’s electoral base but also serves to extract concessions without committing to prolonged escalation.

Vice President J.D. Vance reinforced this posture Sunday, saying the United States “holds more cards” but urging China to “choose the path of reason.”

That dual message — confrontation combined with an invitation to negotiate — mirrors the approach used in previous trade standoffs.

China’s Position: Flexibility With Leverage

Beijing’s new rare-earth licensing rules provide leverage without triggering immediate supply disruption. They do not ban exports; instead, they require case-by-case approvals for shipments involving sensitive applications such as semiconductors and defense.

This structure gives Chinese authorities discretion to slow shipments selectively while maintaining compliance with World Trade Organization rules. It also leaves room to ease or tighten controls depending on the tone of U.S. policy.

Chinese officials emphasized that the rules were adopted under the Foreign Trade Law and Export Control Law, both of which allow such measures for national-security reasons. The Ministry of Commerce reiterated that “China does not seek confrontation but will defend its interests.”

That language, measured but firm, suggests China intends to use timing and administration rather than blanket bans — an approach that tends to generate uncertainty but not immediate economic loss.

Supply-Chain Realities

Rare earths are indispensable to advanced technology manufacturing. The 17 elements in this group appear in electric-vehicle motors, wind turbines, radar systems, and missile guidance.

The United States Geological Survey (USGS) estimates that global demand will grow roughly 8 percent annually through 2030.

China currently accounts for about:

- 60 percent of mining output,

- 90 percent of refining and separation capacity, and

- 93 percent of permanent-magnet manufacturing.

Although the United States, Australia, and Canada have restarted several mines — including MP Materials’ Mountain Pass facility in California — the refining bottleneck remains predominantly in China. The U.S. Department of Defense has invested more than $600 million since 2021 to expand domestic processing, but new plants are years from full operation.

That dependency gives China leverage but also limits how far it can push. Cutting exports too aggressively would hurt its own manufacturers and accelerate the diversification of supply.

Economic Impact: Measured, Not Systemic

Economic models from Oxford Economics and the Peterson Institute suggest that a full 100 percent tariff on Chinese goods could shave between 0.2 and 0.4 percentage points from U.S. GDP over twelve months if sustained. However, that assumes tariffs stay in place and no compensatory policy relief occurs.

For China, the estimated hit would be slightly larger — roughly 0.5 percentage points of GDP — because exports remain a bigger share of output. Yet even those figures would not imply recession in either country.

More importantly, investors have seen similar forecasts before. When the first round of tariffs was announced in 2018, consensus GDP-impact estimates were roughly twice as large as what ultimately occurred. Global trade volumes slowed temporarily but resumed growth within a year.

Evidence of Limited Spill-Through

Forward-looking indicators do not yet reflect meaningful damage:

- Baltic Dry Index, a proxy for shipping demand, is down less than 3 percent since the announcement — well within weekly volatility.

- Copper prices, often an early signal of industrial demand, remain above $8,200 a ton, unchanged from early October.

- Corporate bond spreads in the U.S. investment-grade market widened by just 4 basis points, far below stress thresholds.

These data points suggest financial markets are reacting to uncertainty rather than deterioration in trade flows or production.

Investor Considerations

Given these dynamics, investors face three key questions:

1. Will tariffs be implemented as stated?

Historical precedent suggests probability remains low until formal documentation appears. Monitoring the U.S. Trade Representative’s filings and Chinese licensing enforcement will provide early confirmation.

2. Are corporate earnings at risk?

Sector exposure is uneven. Electronics and autos face the largest potential input-cost pressures, while financials and energy are relatively insulated. Analysts have not yet revised Q4 earnings estimates, indicating limited concern so far.

3. Is this a buying opportunity or a warning sign?

Empirical studies from J.P. Morgan and Goldman Sachs during previous tariff cycles found that buying after 3-to-5 percent trade-related pullbacks generated positive three-month returns more than 70 percent of the time, provided no actual policy escalation followed.

What to Watch Next

- Official tariff notice: The U.S. Federal Register publication would mark a concrete step beyond rhetoric. None has been filed yet.

- China’s licensing pace: Customs data for November exports will reveal whether shipments slow materially.

- Diplomatic scheduling: Reports of another bilateral trade meeting would likely calm markets quickly.

Until one of those factors shifts, current volatility should be interpreted as a short-term sentiment response, not a change in macroeconomic fundamentals.

Conclusion

The episode highlights how financial markets have become hypersensitive to policy communication, reacting within minutes to statements that may never translate into law. That sensitivity reflects liquidity, automation, and investor memory of past crises — not necessarily rational assessment of risk.

If history is a guide, once the rhetoric cools, valuations tend to revert to levels consistent with earnings and interest-rate expectations. The underlying picture — moderate global growth, easing inflation, stable employment — remains intact.

For investors, the more reliable course is to focus on data that move profits and productivity, not the noise that moves headlines.

Take the Next Step: Strengthen Your Strategy Amid Market Volatility

Periods of sharp market swings — like the recent reaction to Trump’s 100% tariff threat — can test even well-built portfolios. The key isn’t to react impulsively, but to refine your exposure to risk, review diversification, and ensure your holdings align with long-term objectives.

With clear insight and disciplined allocation, temporary volatility can become an opportunity to reinforce portfolio resilience and position for steadier growth ahead.

This article is for general information only and does not constitute financial, legal or tax advice. Rules, prices and regulations change; verify current requirements with a qualified adviser before acting.