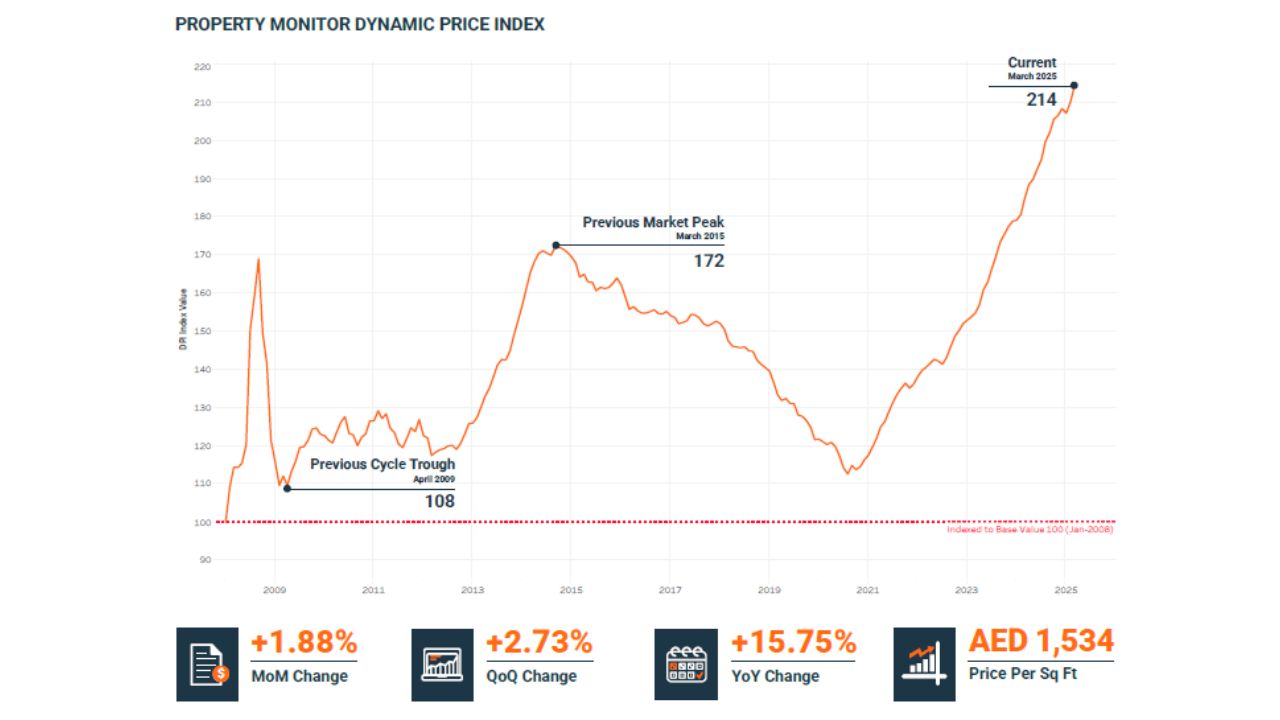

Dubai property prices continued their upward trajectory in March 2025, with a 1.88% increase in the Dynamic Price Index (DPI). This marks the second consecutive month of above-average growth, pushing average prices to AED 1,534 per sq ft. That’s 24.3% above the previous market peak in September 2014.

The consistency of this trend, now 53 months into the current cycle, highlights market maturity but also calls for greater precision in investment decision-making.

The historical context is key. In the 2012–2014 cycle, price growth averaged 1.6% per month, peaking at 2.99%. In contrast, this cycle’s monthly appreciation has averaged 1.2%, with a peak of 2.51%. **The current pace **is slower but more resilient, indicating stronger fundamentals, broader demand, and less reliance on speculative flows.

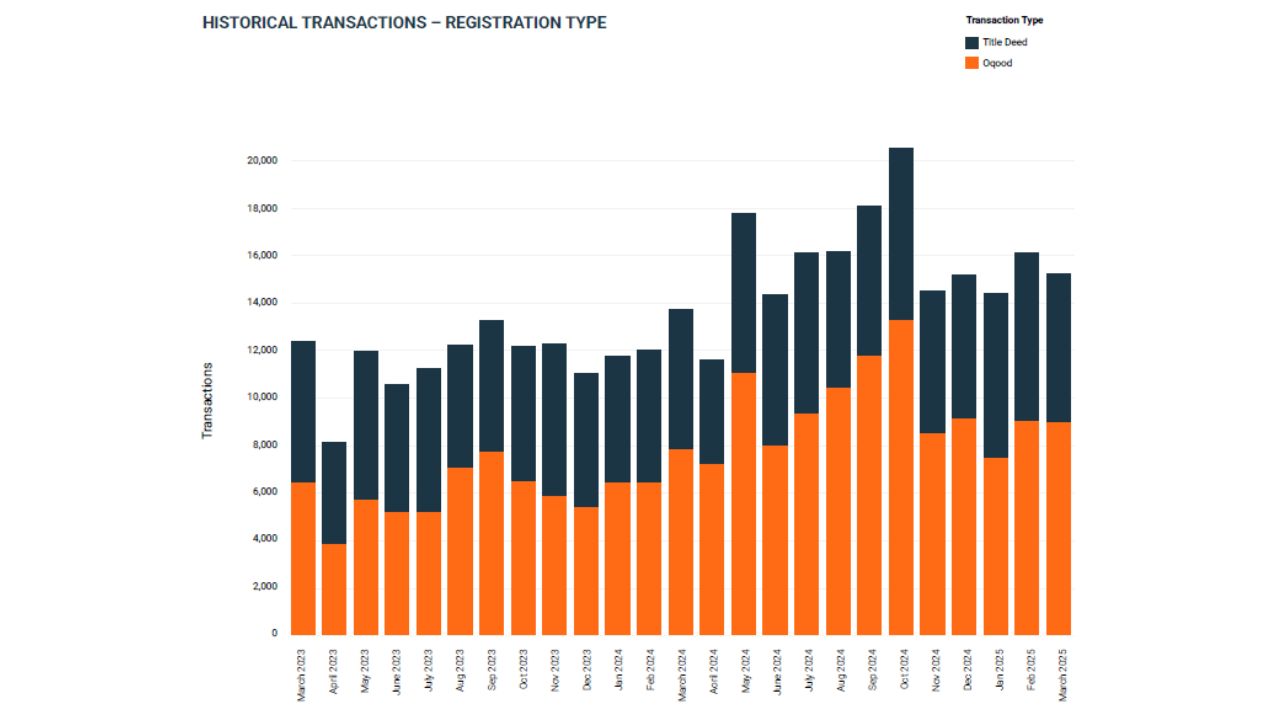

Record Transaction Volume Despite Fewer Trading Days

While overall transaction volumes declined 5.7% month-on-month, March still delivered 15,223 sales, making it the strongest March on record—11% above March 2024. The dip can largely be attributed to fewer trading days during the Eid break, rather than a downturn in market appetite.

Residential transactions dominated the landscape, comprising 93.7% of the total (14,274 deals). Apartments, villas, and townhouses remain the clear drivers of demand. Commercial properties—including offices (2.1%), land (1.5%), and hotel apartments (1.0%)—continued to play a minor role, consistent with ongoing investor focus on income-generating residential assets.

Image Credit: Property Monitor

Off-Plan Dominates With Expanding Market Share

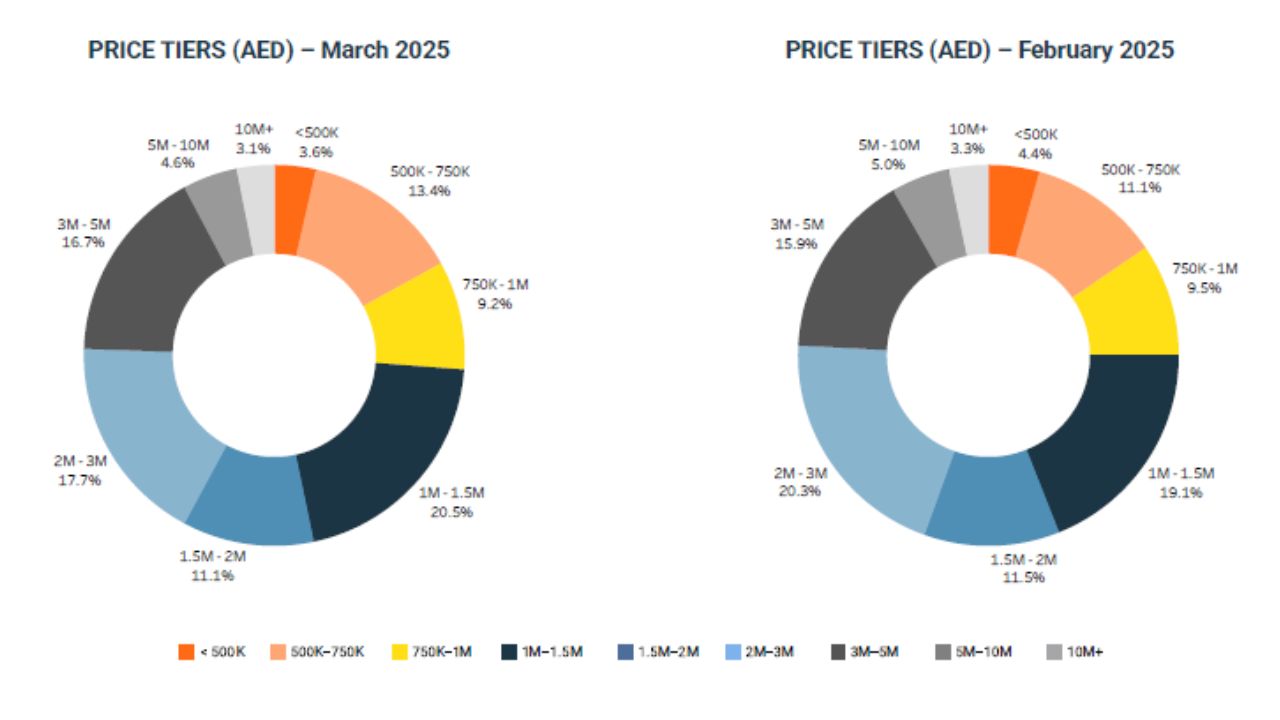

Off-plan remains the most active segment, with off-plan transactions representing 67.2% of all sales after technical adjustments for reporting discrepancies. Official Oqood transactions recorded 9,005 off-plan deals, reflecting just a 1% dip from February. The off-plan market has shown not only volume strength but also pricing power, consistently outperforming the ready property segment.

In 14 out of the 42 communities tracked, off-plan price premiums exceeded 30%, with standout gaps of 85% in Motor City and 73% in Dubai Sports City. These figures reveal a clear quality disparity between new developments and older stock—especially in areas where older properties lack modern finishes, amenities, and layouts. Investors are increasingly willing to pay a premium for newer product, especially when developers offer phased payment plans and attractive incentives.

Ready Property Activity Slows Under Competitive Pressure

Ready property sales declined by 11.7% month-on-month, now accounting for 40.8% of the market. While this may appear concerning on the surface, the dip coincided with fewer working days in March. More significantly, the trend reflects competitive pressure from off-plan launches, many of which offer superior specifications and more flexible financial terms.

That said, the ready segment still presents value opportunities, particularly for investors prioritizing immediate rental income or looking to avoid handover uncertainty. Select communities with strong maintenance reputations and infrastructure continue to show price stability and rental resilience.

Resale Activity Rises, Signaling Portfolio Adjustments

Resale transactions increased to 6,514 in March, up 1.4% from February, now representing 42.8% of the total market. This rise in resale activity reflects a maturing cycle, with more investors repositioning holdings or exiting after capturing capital appreciation.

Notably, off-plan resales made up 29.3% of these deals, up from the 12-month rolling average of 25.4%. Most resales occurred in projects within 12 months of handover, suggesting these exits are strategic—targeting liquidity or rotating capital into newer launches.

Image Credit: Property Monitor

However, the emerging pattern of resales 15–16 months ahead of handover indicates a broader shift. Whether this reflects speculative flipping or preemptive de-risking will depend on how this trend evolves over the next two quarters.

Mortgage Market Realigns Toward End Users and Smaller Investors

Mortgage activity declined 2.3% to 3,434 loans, though the composition of borrowing shifted meaningfully. Purchase money mortgages rose to 56.9% of total lending, up 6.3% from February, signaling renewed momentum among end users and mid-sized investors.

The average mortgage size in March was AED 1.88 million, with a loan-to-value ratio of 75.6%, indicating continued prudent leverage behavior. Refinancing and equity release accounted for 36.3% of loans, while bulk mortgage volumes dropped to 6.8%, down 7.6% month-on-month.

Bulk mortgage activity was largely concentrated in a few key projects:

- Orra Harbour (49 units)

- Orra Marina (21 units)

- RP Heights (20 units)

The decline in developer and institutional borrowing suggests a slightly more cautious stance on large-scale acquisitions, or simply a return to more organic sales growth via end-user and retail investor demand.

Absorption Rates Strong, But Saturation Signs Emerge

The market continues to absorb new supply at an impressive rate, particularly in the off-plan segment. However, there are early signals that launch velocity is beginning to outpace absorption capacity in certain communities. As more projects move from initial sales to later phases, investor scrutiny is intensifying.

Communities with multiple concurrent launches—particularly in the mid-market apartment segment—are most vulnerable to saturation. When too many similar units are released simultaneously, absorption slows, and developers are forced to compete more aggressively on price or incentives. Investors entering these micro-markets now must account for future competition at handover, both in rental terms and resale potential.

The key to navigating this shift lies in targeting differentiated supply. Projects that offer distinct layouts, upgraded common areas, curated amenities, or integration with retail and transit infrastructure are best positioned to maintain pricing power. Investors should look beyond launch pricing and evaluate handover period demand, as well as surrounding pipeline volume.

Investor Behavior: From Opportunistic to Selective

Over the past year, investor sentiment has evolved from opportunistic entry to selective optimization. The early stages of the cycle (2020–2022) were marked by aggressive accumulation, with price discovery playing out across a wide swath of projects and sub-markets. In 2024 and into 2025, we’re seeing more refined capital deployment, where timing, quality, and holding period strategy are paramount.

Resales of off-plan units close to handover are being used to monetize gains and de-risk portfolios. Meanwhile, new positions are increasingly focused on developers with a strong track record, or on neighborhoods where rental demand is forecast to grow with infrastructure and population expansion.

Early off-plan resales—those with over 15 months remaining—are more mixed in motivation. Some investors are seeking early exits due to concerns about price ceilings in saturated zones. Others are simply reallocating toward shorter-cycle assets or looking to exit as global financial conditions tighten. Either way, the pattern reflects a more active, data-driven investor mindset than seen in past cycles.

Cyclical Maturity Requires Strategic Patience

Dubai’s current market cycle is entering a mature phase. Price growth remains positive but is moderating in select areas. Investor interest is strong, but increasingly focused on defined niches, such as waterfront properties, branded residences, or townhouses in lifestyle-oriented master communities.

Those looking to enter or expand their holdings now must prioritize resilience over rapid appreciation. That means:

- Choosing developers with transparent pricing and on-time delivery histories.

- Avoiding communities where five or more similar projects are set to hand over within the same year.

- Factoring in exit timelines based on handover, payment plan milestones, and anticipated supply curve shifts.

How the March 2025 Property Monitor Report Informs Smart Evaluation of Developer Strategy

The latest data makes one thing clear: while demand in Dubai’s real estate market remains strong, absorption is becoming more selective. In certain communities, especially those with multiple overlapping off-plan launches, supply is beginning to test demand capacity.

For investors, this underscores the importance of evaluating not just the asset—but also the developer's approach. Projects rolled out without pricing discipline or phased planning are more likely to face longer sell-through timelines, inventory overhangs, and margin compression that can affect resale and rental values.

Investors should focus on developers that:

- Launch projects in phased, market-aligned cycles, rather than pushing volume to capture short-term sales headlines.

- Deliver genuine value differentiation—functional layouts, long-term livability, and modern amenities—rather than superficial upgrades.

- Maintain credible delivery timelines and offer payment terms aligned with investor cash flow needs.

A developer’s track record in execution and pricing strategy directly influences an investor's exit options. Those with consistent handover performance and a reputation for build quality tend to generate stronger resale interest, stable rental demand, and lower vacancy risk. In short, developer discipline isn’t just a supply-side issue—it’s a key risk filter and return driver for today’s investor.

Macro Risks Are Contained But Present

Dubai’s market fundamentals remain strong, but external risks are increasing in visibility. Persistent inflation, global rate volatility, and geopolitical uncertainty could weigh on investor confidence later in the year. Although Dubai is largely insulated by regional demand and policy stability, elevated interest rates and higher financing costs may limit leverage-driven investment from certain segments.

Domestically, the main structural risk is oversupply in specific communities, particularly where off-plan launches have outpaced infrastructure readiness or where demand drivers are concentrated in one buyer profile (e.g., bulk investors or short-term speculators).

Mitigating these risks will require investors to build flexibility into their exit strategies, stress-test their financing scenarios, and monitor resale liquidity trends quarterly.

Conclusion: Invest with Focus, Adapt with Data

The March 2025 Property Monitor Report offers a detailed, data-backed confirmation that Dubai’s property market is strong—but transitioning. Transaction volumes remain near historic highs, prices continue to grow steadily, and investor activity is diverse and tactical. At the same time, shifts in off-plan absorption rates, early resales, and selective mortgage trends point to a market that’s becoming more strategic and competitive.

For investors, the path forward is clear: target differentiated products, remain attuned to demand cycles, and prioritize liquidity and quality over momentum. For developers, the message is equally direct: build with purpose, launch with discipline, and deliver with consistency.

Dubai’s market is not cooling—it’s calibrating. Those who recognize the shift early and position intelligently will outperform as the next phase unfolds.

FAQs: Navigating Dubai’s Property Cycle with Confidence as a Strategic Investor

Is Dubai property still a good investment in 2025?

Yes—if approached strategically. The market remains fundamentally strong, but it’s entering a more mature phase. Investors should prioritize differentiated assets, avoid oversupplied areas, and plan for longer holding periods to optimize returns.

Should I invest in off-plan or ready properties right now?

Off-plan remains attractive, especially for projects nearing handover with strong developer reputations. However, ready properties in well-maintained communities offer stable rental yields and immediate cash flow—ideal for income-focused investors. Selection and timing are critical in both segments.

Why are off-plan units commanding such high premiums?

Premiums—up to 85% in some areas—reflect a growing gap in quality between new and older stock. Investors are paying for better layouts, amenities, sustainability features, and flexible payment structures. These assets are more appealing to end users and command stronger resale interest.

What does rising resale activity indicate?

Rising resale volumes—especially for off-plan units—suggest that investors are monetizing gains, reallocating capital, or managing risk ahead of potential saturation. The uptick in resales for units 15+ months from handover could signal cautious repositioning or early exits.

How are interest rates affecting investor financing?

While overall mortgage volumes dipped, purchase loans increased—showing end users and yield-driven investors remain active. Bulk borrowing by large investors declined, indicating a shift toward more organic, smaller-ticket purchases. Fixed-rate options are gaining popularity amid rate volatility.

Are there signs of oversupply I should be concerned about?

Yes, in select mid-market apartment zones with multiple overlapping launches. Watch for areas where handovers are clustered and infrastructure is still developing. Assess future rental competition and resale timelines before committing capital.

How should I evaluate developers when buying off-plan?

Developer credibility directly impacts exit value. Look for:

- Timely, consistent handovers

- Realistic pricing strategies

- Thoughtful phasing and community integration

Well-managed projects tend to attract stronger post-handover demand and minimize vacancy risk, supporting both capital appreciation and rental performance.

What risks should I be factoring into my investment decisions?

- Localized oversupply in fast-launching zones

- Rising financing costs

- Geopolitical uncertainty impacting global capital flows

- Shift from broad-based to selective demand

Portfolio decisions should incorporate liquidity planning, hold period stress testing, and data-driven community comparisons.

Speak With Me Directly – Let’s Build Your Dubai Investment Strategy

If the insights in this report resonate with your goals, let’s explore how they apply to your portfolio. Whether you're entering the Dubai market or scaling an existing position, I offer tailored, data-backed guidance to help you move with clarity—not noise.

From identifying credible off-plan opportunities to optimizing asset allocation in a shifting cycle, I provide strategic advice rooted in experience—not speculation.

Visit My Site to Explore More In-Depth Reports, Market Commentary, and Strategic Guidance Tailored for Serious Investors.

Let’s Connect with a confidential, no-obligation conversation—if you’re ready to turn insight into action.

As the Managing Director of Global Investments, I bring 25+ years of expertise in finance, wealth management, and real estate. I specialize in portfolio diversification, deal structuring, and wealth preservation, delivering data-driven strategies for sustainable success in global markets.

This article is for general information only and does not constitute financial, legal or tax advice. Rules, prices and regulations change; verify current requirements with a qualified adviser before acting.